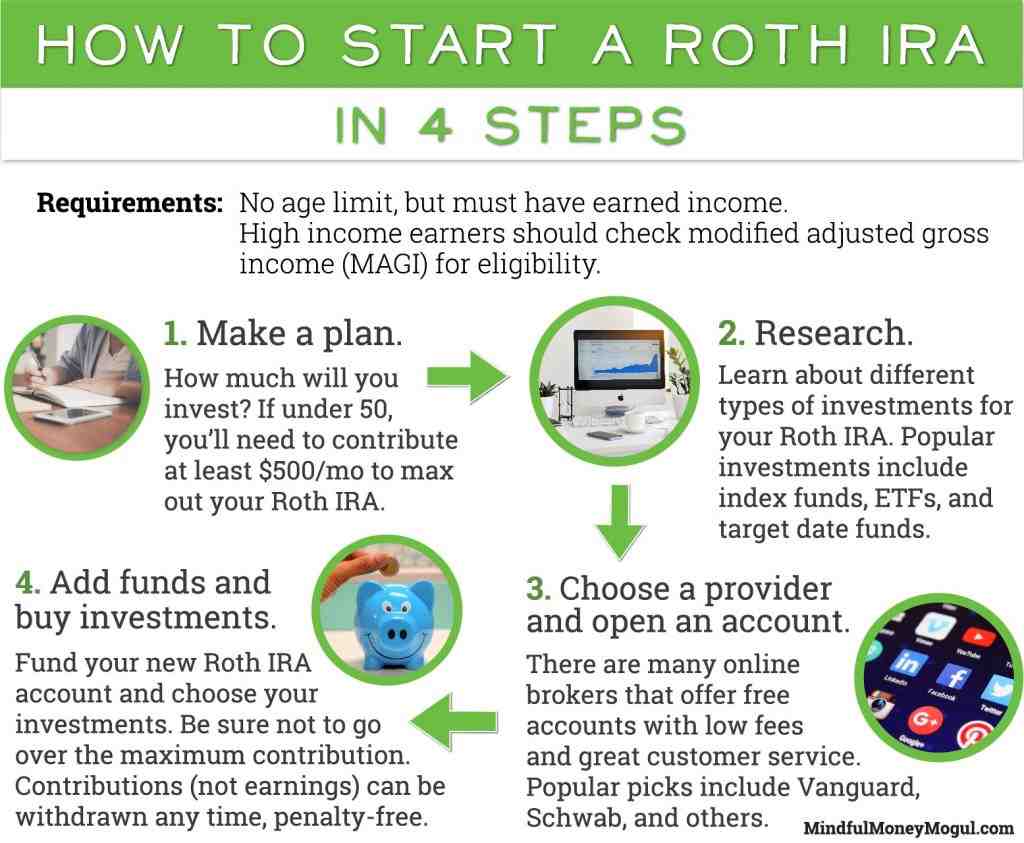

How Much Can I Convert From Traditional IRA To Roth IRA?

Converting funds from a Traditional IRA to a Roth IRA is a significant financial decision that can have lasting implications on your retirement savings. Understanding how much you can convert is crucial for effective tax planning and maximizing your retirement funds. This article will explore the various factors influencing the conversion process, including tax implications, contribution limits, and strategies to minimize tax burdens. By the end, you will have a comprehensive understanding of how much you can convert and the best practices to follow.

The decision to convert from a Traditional IRA to a Roth IRA is not just about current finances; it requires a strategic outlook on your long-term retirement goals. Factors such as your current tax bracket, expected future income, and overall financial situation can significantly impact how much you should consider converting. Additionally, the IRS has specific rules and regulations that govern these conversions, making it essential to be well-informed before proceeding.

This article is organized to provide you with a thorough understanding of the conversion process. We will cover the benefits and drawbacks of converting to a Roth IRA, the mechanics of the conversion, and the factors you need to consider before making the leap. Let's dive into the details to empower your financial decision-making process.

Table of Contents

- Benefits of Roth IRA

- Tax Implications of Conversion

- How Much to Convert?

- Strategies for Conversion

- Conversion Limits and Rules

- Impact on Future Taxes

- Conclusion

- Call to Action

Benefits of Roth IRA

A Roth IRA offers several advantages that make it an attractive option for retirement savings:

- Tax-Free Growth: Earnings in a Roth IRA grow tax-free, meaning you won't owe taxes on qualified withdrawals in retirement.

- Flexible Withdrawals: Contributions can be withdrawn at any time without penalties or taxes, providing flexibility in financial planning.

- No Required Minimum Distributions (RMDs): Unlike Traditional IRAs, Roth IRAs do not require you to take distributions at a certain age, allowing your money to grow longer.

- Tax Diversification: Having both Roth and Traditional accounts can provide tax diversification in retirement, allowing for strategic withdrawals based on your tax situation.

Tax Implications of Conversion

Converting from a Traditional IRA to a Roth IRA has significant tax implications:

- Taxable Income: The amount you convert will be added to your taxable income for the year, potentially pushing you into a higher tax bracket.

- State Taxes: Depending on your state, you may also owe state taxes on the converted amount, which should be factored into your decision.

- Impact on Other Benefits: A higher taxable income could affect eligibility for certain benefits or credits.

How Much to Convert?

Determining how much to convert from a Traditional IRA to a Roth IRA involves several considerations:

- Your Current Income: Assess your current income and tax bracket, as this will influence how much you can convert without incurring excessive taxes.

- Future Income Expectations: Consider your expected income in retirement. If you anticipate being in a higher tax bracket, converting more now may be beneficial.

- Retirement Timeline: The longer you have until retirement, the more time your money has to grow tax-free in a Roth IRA.

Factors to Consider for Conversion Amount

Here are some additional factors to consider:

- Your overall financial situation

- Other sources of retirement income

- Your tax situation and planning

- Market conditions and investment performance

Strategies for Conversion

To maximize the benefits of converting to a Roth IRA, consider the following strategies:

- Partial Conversions: Instead of converting your entire Traditional IRA at once, you can opt for partial conversions over several years to manage tax implications.

- Convert in Low-Income Years: If you anticipate lower income in certain years, those may be ideal times to convert more funds.

- Utilize Tax Credits: If you qualify for tax credits or deductions, use those to offset the tax liability from the conversion.

Conversion Limits and Rules

While there are no limits on how much you can convert, there are rules to be aware of:

- Income Limits: There are no income limits for conversions, but your tax liability may increase based on the amount converted.

- Five-Year Rule: To avoid penalties on converted amounts, you must wait five years before withdrawing earnings from the converted account.

Impact on Future Taxes

Converting to a Roth IRA can influence your future tax situation:

- Retirement Withdrawals: Qualified withdrawals from a Roth IRA are tax-free, which can be advantageous in retirement.

- Estate Planning: Roth IRAs can be beneficial for estate planning as heirs can inherit funds without immediate tax consequences.

Conclusion

In conclusion, converting from a Traditional IRA to a Roth IRA can provide substantial tax benefits and flexibility in retirement. However, determining how much to convert requires careful consideration of your current financial situation, future income expectations, and tax implications. By understanding the rules and strategies associated with this conversion, you can make informed decisions that align with your long-term financial goals.

Call to Action

If you found this article helpful, please leave a comment below, share it with others, or explore more articles on our site for additional insights on retirement planning and investment strategies.

Thank you for reading, and we hope to see you back soon for more valuable information!

Discovering Sonneberg: The Hidden Gem Of Germany

Can You Put Protein Powder In A Smoothie? Exploring The Benefits And Best Practices

Cancer And Pisces Friendship Compatibility: A Deep Dive

{kind=link}